The pandemic drove massive increases in the adoption of food and grocery delivery and meal kit services, forcing us to think differently about how and where we purchase food. But, as we wade through a post-lockdown world, will consumers keep having food delivered at the same rate?

In early 2020, COVID-19 rocked the world.

As the world plunged into lockdowns, we all did our best to limit social gatherings, making the collective decision to pause some of our favorite pastimes. Having dinner parties, going to bars and restaurants to celebrate birthdays, or lounging around the house with friends all ground to a halt. This change drove many of us to test meal kits and order from our local restaurants through delivery apps. And some wanted or needed to keep their distance even more, opting to get groceries delivered to protect themselves or loved ones.

Food delivery in some form or another isn’t new. But global lockdowns massively increased the adoption of these services. As we wade through a post-lockdown world, will consumers keep having food delivered at the same rate? To what extent are we eager to shift back to going out to eat, getting off our sofas and exploring the outside world?

The time periods, information, and definitions

Our friends over at Drop provided us with transactional data to see the trends pre-lockdown, during lockdown, and post-lockdown across Canada and the US. Many thanks to Drop for supplying this data. And before we get into the juicy stuff here is some extra information on the time periods and which food delivery industries we looked at.

The periods are slightly different per country because of the lifting of regulations. We’ve defined the different time periods as follows:

Pre-lockdown is from January 2019 to February 2020. This helped us determine what the market looked like before.

Lockdown is from March 2020 to June 2021 in the US and from March 2020 to December 2021 in Canada.

Post-lockdown is from the end of those periods to June 2022.

The user base for the US was more than 150,000 people. The Canadian user base was smaller, sitting in at just over 10,000 people which could skew some of the data. However, with few exceptions, most trends held true across both countries.

Food delivery often means ready-to-eat food from restaurants delivered directly from the restaurant or through a third-party app like UberEats. Grocery delivery is similar but is often outsourced to a third party. Meal kits are heat-and-serve or cook-and-serve meals often dispatched through the meal kit company.

A look at the past – pre-lockdown

There was nominal revenue growth across all three delivery services in the US leading up to the beginning of the pandemic. Canada saw slow growth in meal kits during the same period. However, there was already high growth in food and grocery delivery. Possibly a coincidence, or maybe Canada was just a bit earlier adapting to these methods than the US.

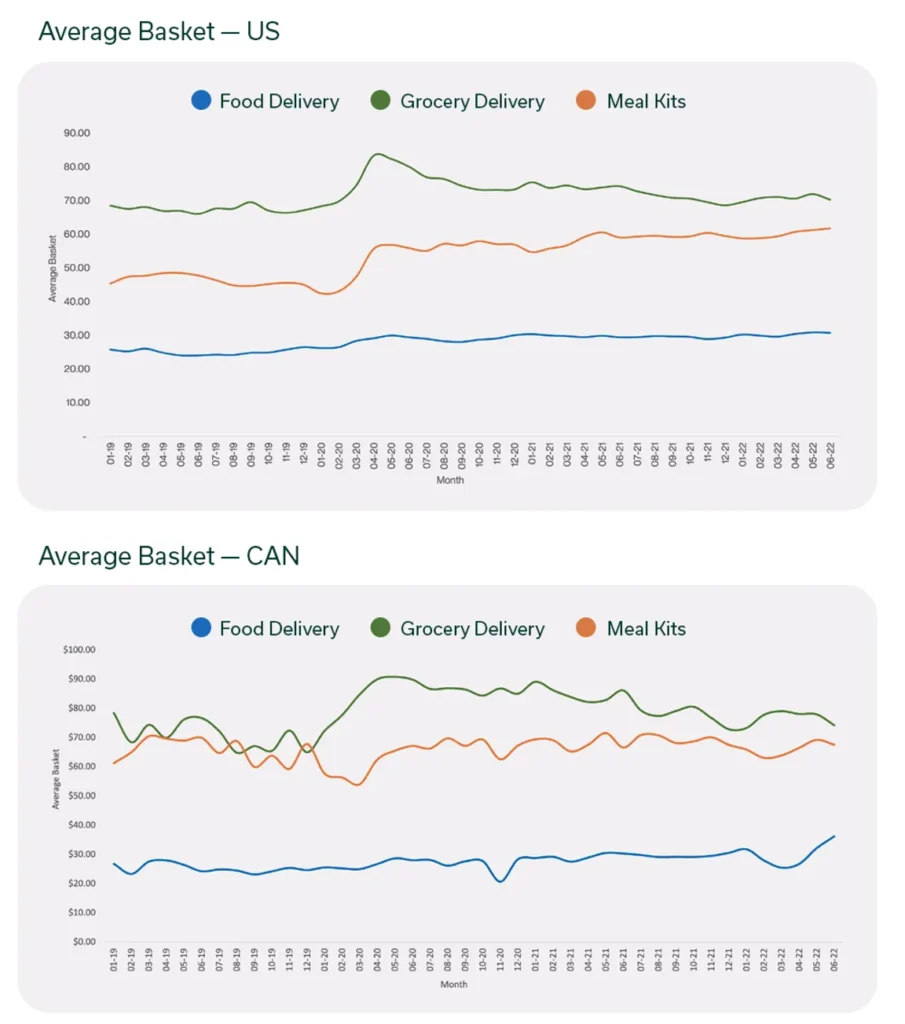

The average cost of an order for each delivery method remained flat across the US. It was mostly the same in Canada. However, grocery and meal kits declined a bit leading into the pandemic.

The purchase frequency over a month was almost identical between the two countries. On average, consumers made 3.5-3.6 food delivery purchases and 2.1 meal kit purchases per month. There was a slight variance in grocery delivery as the US consumer had 2.7 grocery deliveries per month compared to Canada’s 3.2 deliveries.

The average amount spent per customer per month for all services remained flat or only had small growth between January 2019 and February 2020.

Mostly, these industries were slowly growing in the leadup to the pandemic. Not by crazy numbers, which would eventually be the case during the pandemic, as Instacart said it achieved its 2022 goals during the third week of lockdowns (April 2020). And more than a third of American consumers that used grocery delivery services started because of the pandemic.

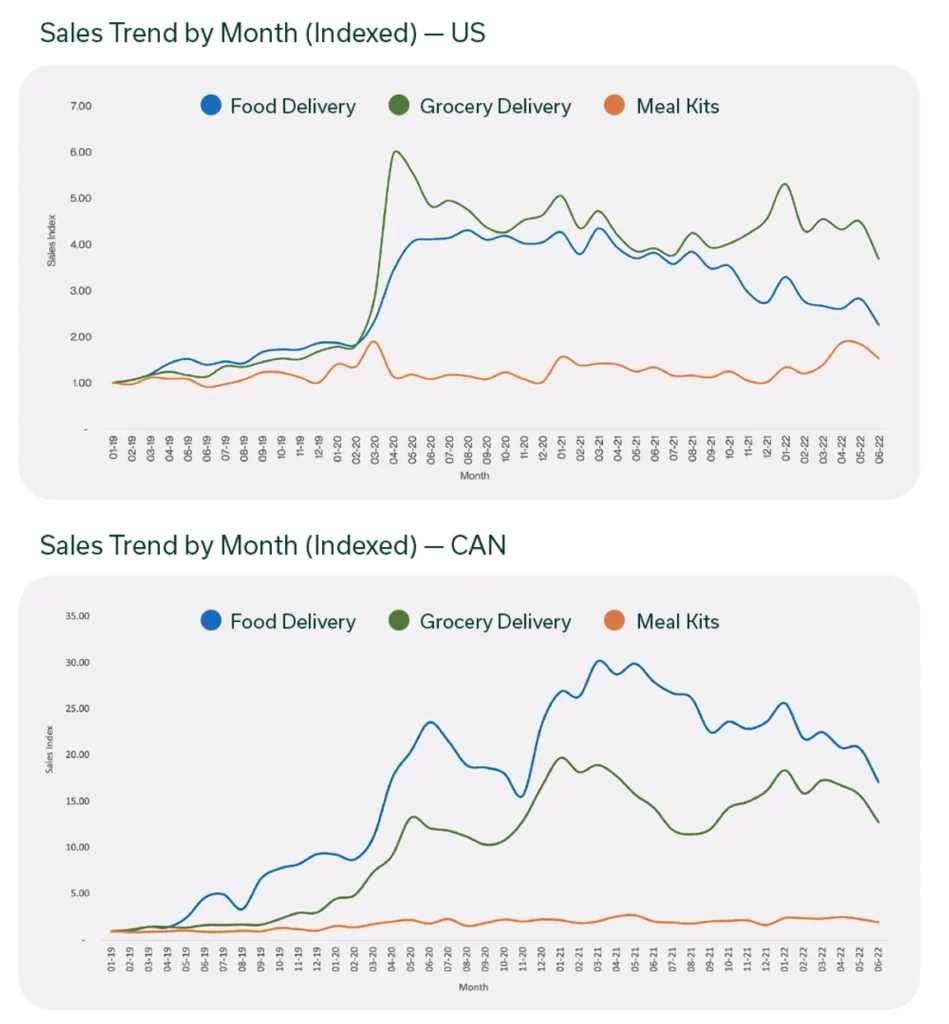

These graphs show the revenue levels for the three delivery services indexed to January 2019. So, January 2019 represents 1 and all increases or decreases are measured based on this number. So, in the US data, you can see that grocery delivery revenue peaks at about 6 times more than it was in January 2019.

A shifting landscape – a.k.a. pandemic growth

As we’ve already hinted at, the pandemic and lockdowns skyrocketed usage of all delivery services. Revenue massively increased during this period. In the US, grocery delivery averaged the highest increase in revenue at 4.55 times more than Jan 2019 (or 232%), while food delivery was a close second at 3.91 times more than Jan 2019 (or 159%). Meal kits did increase during this time, but not as dramatically, increasing revenue by 15%.

In Canada, however, each delivery method had massive growth. Grocery delivery saw a 522% increase in revenue, food delivery a 347% increase, and meal kits had a 92% increase compared to Jan 2019. What’s interesting here is there was a second peak for Canadian consumers. While it’s understandable to see an initial jump across both countries in March of 2020, Canadian consumers had to deal with more lockdowns. This caused them to reach a peak in monthly revenue during the first half of 2021.

The average order value for US consumers increased by 12-23% across the three delivery methods compared to pre-lockdown. In Canada, meal kit and food delivery order values increased 3-9%, respectively. Grocery delivery trends in Canada mimicked the US market, with the average order value increasing by 21% compared to pre-lockdown.

Similarly, frequency and average spend increased throughout lockdown periods. Probably the biggest change was the frequency at which people ordered restaurant delivery. In the US, frequency of food delivery increased by 42%, and in Canada, it increased by 60% compared to the pre-pandemic average.

People still wanted to eat from their favorite restaurants while in lockdown, so they ordered delivery more frequently to support local businesses (and get their fix). But the drastic increase in revenue of grocery delivery across the two countries shows just how underutilized that offering was before the pandemic. The sneaky winner was probably meal kit companies since these trends rose at a more gradual rate, which is likely why post-lockdown, these companies saw numbers level off a bit more subtlety as compared to the other two delivery methods, which saw more drastic declines.

Average basket size refers to the average amount a customer spends for a single purchase. In the US, the average cost per order of meal kits continued to grow after lockdowns. In Canada, you see a bit of a similar trend, but food delivery seemed to be the bigger winner here.

Holding ground or sudden declines? The present picture

So, what does transactional data tell us about the current state of food delivery? For the most part, every type of food delivery service declined from peak pandemic levels. It makes sense. It’s not a complicated scenario to play out in your mind. But how much have things declined? Are we back to pre-pandemic levels, or have consumers gotten used to some of these conveniences?

Revenue

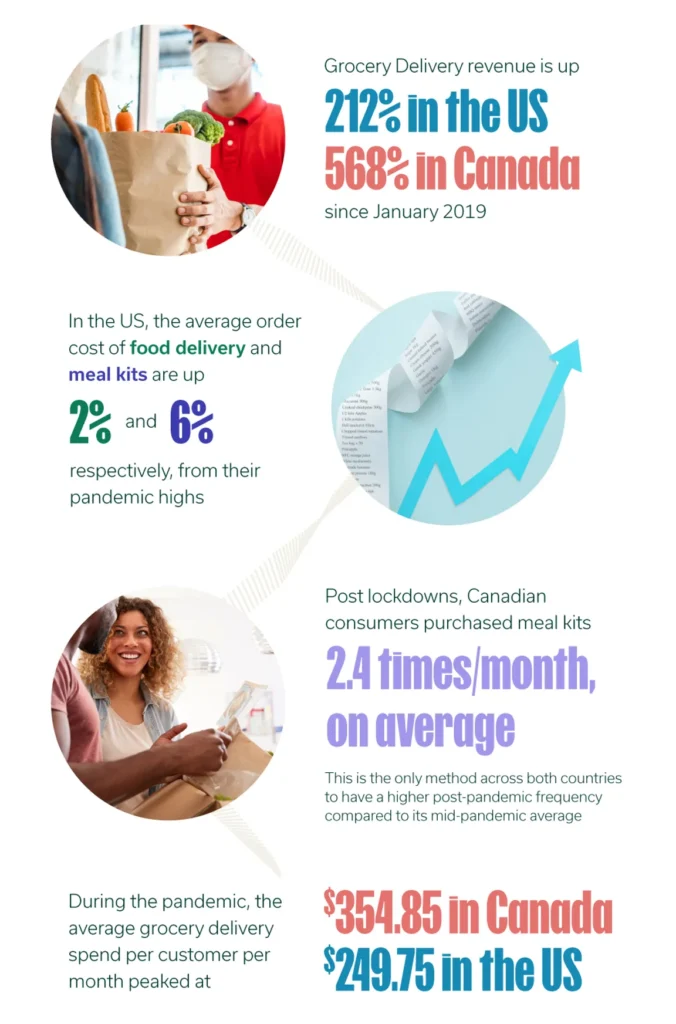

Regardless of country, revenue across all delivery methods is higher than pre-pandemic levels. In Canada, however, the revenue average across the post-lockdown period is actually higher than during the middle of the pandemic. However, it’s on its way down and likely to continue declining. Across both countries, restaurant and grocery delivery take the top two spots, with revenue doubling or tripling the pre-pandemic levels in the US and increasing as much as 560% from pre-pandemic levels in Canada.

Spend

The average grocery delivery order of both countries is lower than it was during lockdowns, but it is still 4-8% higher than pre-pandemic levels. This might mean people aren’t stocking up as much or may be able to get the one-off items in person instead of waiting until their next big order.

Food delivery order value is up 18-19% from pre-pandemic levels in both countries. That equates to an increase of just over $4. Additionally, the average spend is still higher than during lockdowns. In the US, the increased amount compared to mid-lockdown only equates to $0.57. In Canada, it equates to an increase of $2.15.

The average order value of meal kits in the US are up 31% from before the pandemic. However, this is still $3 higher than it was during the pandemic. Canadian meal kit customers are still spending more than before lockdowns (5% increase) and during the pandemic ($1.36 more), but the growth isn’t quite as substantial.

Regardless of the amount, the average cost per food delivery and meal kit order is still higher on average than it was during the pandemic. This likely means that we can expect to see sustained, gradual growth for these two services.

Frequency

The frequency of all delivery methods is down from their pandemic highs. In the US, grocery and meal kit frequency are almost at their pre-pandemic levels (up only 7%). Food delivery frequency is down from the pandemic but is still 23% higher than pre-pandemic levels.

It looks to be trending similarly in Canada for grocery and food delivery. They are both down from their pandemic highs, but consumers are still using them 18% (grocery) and 50% (food) more than prior to the pandemic. The biggest exception is that Canadian consumers are more frequently buying meal kits than they were during the pandemic – now currently up 15% from pre-pandemic levels compared to the 7% increase it had during the pandemic.

In these graphs, frequency is measured by how often consumers make purchases from these services per month. Food delivery remains the highest across both countries. However, it appears to be declining at a faster rate. Regardless, all methods are used more often now than they were prior to lockdowns/the pandemic.

What does this mean, really?

It’s predictable to see a massive influx of these services when the world was thrust into lockdowns. And it’s equally predictable that, as lockdowns and restrictions relaxed, the use of these services would decline. But some additional intriguing consumer trends come out of this hectic time in all our lives.

Where we once had 3-4% of consumers purchasing groceries online a few years ago, as many as 60% of U.S. consumers have purchased groceries online, and over 50% of consumers said they would continue using on-demand grocery delivery services as restrictions lifted.

Similar things can be said about meal kits. They had a massive boom throughout 2020. And they may still be popular among younger generations that don’t have time to cook from scratch, are working multiple jobs, or have dietary restrictions. Approximately 49% of consumers 18-34 say meal kits are part of their weekly grocery routine. However, the industry seems unsure about the future of meal kits. In December 2021, Hello Fresh released their forecast, causing the stock to fall close to 50%. Contrast this with the fact that the CFO of Good Food claims they are seeing record-low levels of churn, which is the rate at which customers opt out of the service entirely. If we combine this with the data from Drop, this checks out; revenue, frequency, average order amount, and average customer spend are still up from pre-pandemic levels.

The curious one to keep an eye on is restaurant food delivery. While the food delivery category has massively expanded, close to 64% of people prefer going to a restaurant to getting delivery. That said, frequency and revenue data suggest food delivery is much more part of our lives than we actually think it is.

So, what’s next? The future of food, grocery, and meal kit deliveries

These technologies and purchasing methods were around before the pandemic and were all growing, some more slowly than others. And others were losing money but anticipating enough growth over time to recoup those losses. The pandemic just sped things up. It drove massive increases in adoption and forced us to think differently about how and where we purchase food.

It looks like some companies are already looking ahead. They recognize they’re in decline, but their futures are still very bright. Meal kit companies are already adding grocery delivery options to their roster of offerings. Maybe in a year’s time you’ll skip your Instacart order and get everything from Good Food or HelloFresh? Or maybe it isn’t about the amount you get delivered from your grocery store, but the speed at which it comes; having an impromptu house party and you forgot an item you need, but don’t have time to return and get it? Maybe a company like Gorillas, offering grocery delivery in a matter of minutes, could be why you choose them moving forward.

Or maybe it’s a combination of subscription services that offer a more sustainable delivery method because they use reusable containers. Or is the need to pick your produce the main deterrent for ordering groceries online? Companies like Robomart plan to send refrigerated autonomous vehicles directly to your doorstep. Maybe that could finally force you to make the switch to grocery delivery.

In addition to understanding why people are still using these services, we hope to find out if some of these new offerings intrigue consumers. So, stay on the lookout for some food, grocery, and meal kit delivery studies.

Until then, we’re eager to see where it all goes.